A funny effect of media conglomeration in Hollywood is that many people, including myself, can use corporate names to signal whether we are speaking about Hollywood studios as producers of films, or as parts of giant media conglomerates. When we talk about this or that movie being produced by Warner Bros., Paramount, or Universal, we name movie studios that do exist, but these are also short-form, “classic” names that help separate cinema talk from business talk. When conversations switch to business, film studios with historical pedigree become what they are on paper, subsidiaries of corporate parents — e.g., Warner Bros. Discovery, Paramount Skydance (formerly Paramount Global), and NBCUniversal.

The effects of media conglomeration in Hollywood, whereby firms in media and entertainment merge or acquire others, are felt in the film industry, as well as by consumers. The effects of American media conglomeration in 2025 have been especially newsworthy. The completion of the Paramount-Skydance merger was entangled with the decision of CBS, a subsidiary of Paramount, to settle Trump’s lawsuit against 60 Minutes. Coincident with the settlement was the FCC’s approval of the Paramount-Skydance merger when it allowed for the transfer of broadcast licenses. The host of CBS’ Late Show, Stephen Colbert, called CBS’s settlement with Trump a bribe for the FCC approval. Three days later, CBS told Colbert that the Late Show was going to be cancelled in 2026.

This and the next series of posts will put the mergers and acquisitions that swirl around Hollywood in a bigger political economic context. There is a valuable reason to do this. Collections of business journalism and academic research on the business of Hollywood will often narrative the history of how mergers and acquisitions made certain media firms gigantic. Yet, often what is missing from writing on media conglomeration are the layers of analysis that can help us see the relative significance of a merger or acquisition strategy.

To be clear, there is excellent writing on the history of conglomeration in Hollywood; I will include some in the bibliography below. However, mergers and acquisitions in Hollywood have always been situational, relative to what else is happening in the film industry, as well to what is happening more broadly, in other sectors.

Constructing a buy-to-build indicator for Hollywood

Looking at a merger or acquisition in isolation can produce an explanation that has succumbed to a common fallacy in economic theories of productivity. The fallacy involves using an observable price to explain the productive cause of the price, which can never be measured directly. For example, the sale price of a merger or acquisition in media — say $100 million for the acquisition — can appear to signal the value of the past productivity of creative inputs. For example, in a paper on the brand value of YoutTube, Willmott moves backward to explain the price Google paid to acquire YouTube:

YouTube was acquired by Google for $1.65bn in 2006 when it had just 65 employees. That is a potent illustration of how the labour of user-consumers built the brand equity of YouTube that was turned into brand value. The proceeds of the sale of YouTube were shared amongst those legally credited with owning the site … to the exclusion of those who provided its content and built its reputation. The capitalist state ensured that, legally, the co-producers of YouTube’s brand equity had no entitlement to the dollar value generated by their labour.

Willmott, H. (2010). Creating ‘value’ beyond the point of production: branding, financialization and market capitalization. Organization, 17 (5), 517–542.

Willmott is updating a Marxist theory of appropriation: the shareholders of YouTube were making it rich on the appropriation of labour time, which in this case came from the users that made and uploaded content for free. The suggestion that Google paid $1.65 billion for the sum of all contributing productivity, however, must also imply that YouTube’s users could have been paid for their inputs — how else would we know that a magnitude of user activity (e.g., hours, number of videos, likes) contributed to the $1.65 billion? But as with other processes in modern industry, the labour of cultural goods cannot simply be deconstructed into atomistic, definable factors of a production function. The complexity of modern industry and the mixture of different commodities in the same production processes blur the lines that would allow us to say that each input contributed a definite quantity of value.1

Furthermore, what does a company like Google want when it purchases YouTube? Once again, economic theories can be caught playing theoretical tricks with what can be observed. For example, Nitzan and Bichler’s explain how Ronald Coase’s theory of transaction costs will say “efficiency” no matter what a firm does, whether it internalizes production costs through consolidation or purchases from the market:

The ideological leverage of this theory proved immense. It implied that if companies such as General Electric, Cisco or Exxon decided to ‘internalize’ their dealings with other firms by swallowing them up, then that must be socially efficient; and it meant that their resulting size – no matter how big – was necessarily ‘optimal’ (for instance, Williamson 1985; 1986). In this way, the nonexistence of perfect competition was no longer an embarrassment for neoclassical theory. To the contrary, it was the market itself that determined the right ‘balance’ between the benefits of competition and corporate size – and what is more, the whole thing was achieved automatically, according to the eternal principles of marginalism.

Nitzan, J., & Bichler, S. (2009). Capital as Power: A Study of Order and Creorder. New York: Routledge.

But then, there is a little glitch in this Nobel-winning spin: it is irrefutable. The problem is, first, that the cost of transactions (relative to not transacting) and the efficiency gains of transactions (relative to internalization) cannot be measured objectively; and, second, that it isn’t even clear how to identify the relevant transactions in the first place. This measurement limbo makes marginal transaction costs – much like marginal productivity and marginal utility – unobservable; and with unobservable magnitudes, reality can never be at odds with the theory.

By rejecting the productivity explanation of mergers and acquisitions, Nitzan and Bichler reject what follows in the explanation’s wake: a dance that tries to deconstruct the efficiency gains of different mergers or acquisitions. Their buy-to-build indicator is an important step to understanding mergers and acquisitions as the consolidation of the control of efficiency, not efficiency as such. The buy-to-build indicator is the ratio of the dollar value of mergers and acquisitions to the dollar value of gross fixed investment (Nitzan & Bichler, 2009, p.338). The ratio helps us see, empirically, the extent that business consolidation is a substitute for spending on production. Mergers and acquisitions overshadow production as the ratio rises, and green-field growth has its day in the sun when the ratio falls.

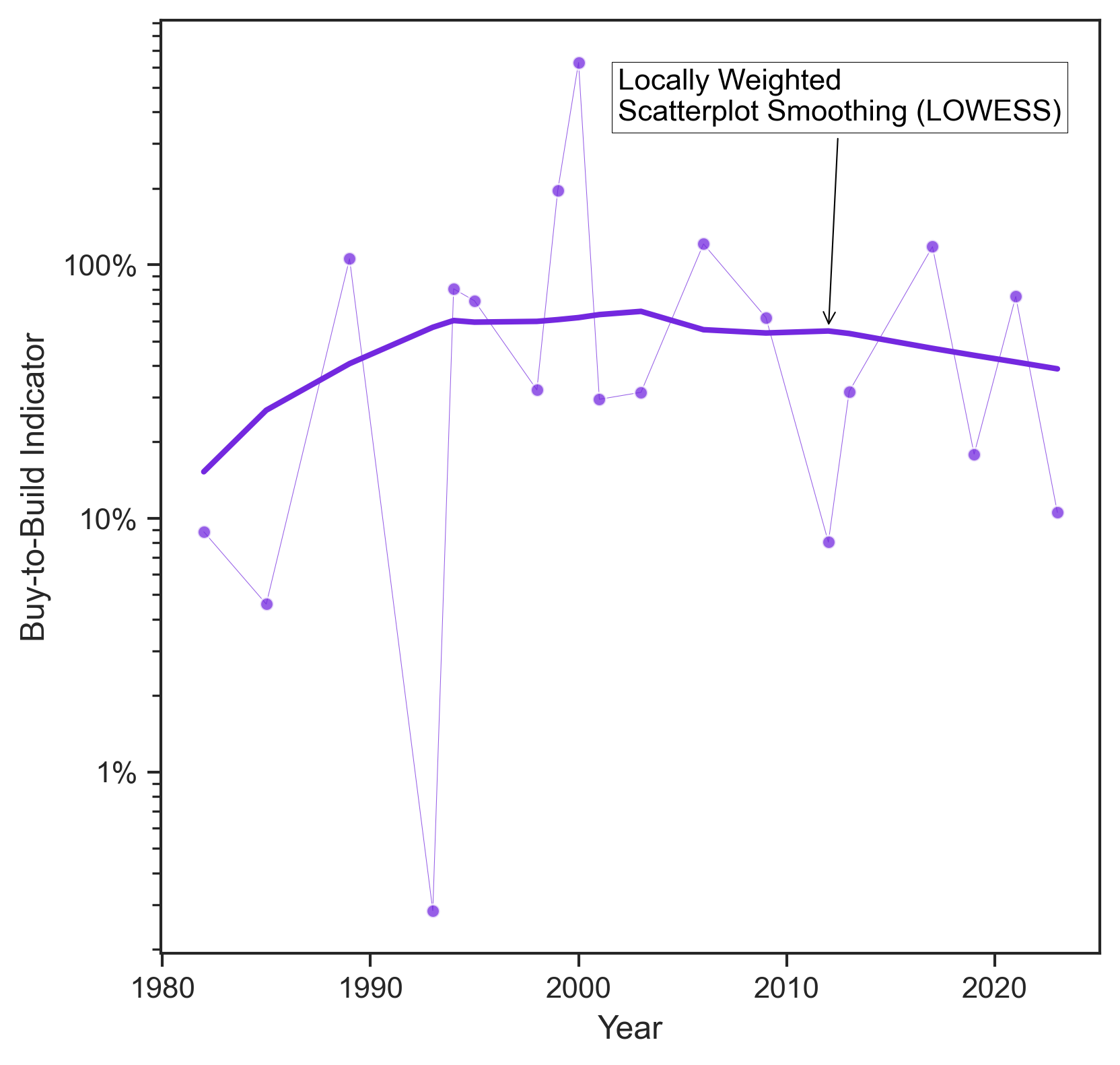

Figure 1 presents my first version of a buy-to-build indicator for the Hollywood film and television sector. The numerator of the ratio — the “buy” — is the dollar value of major2 mergers and acquisitions in American film and television.3 The “build” is the sum of private fixed investment4 in movies and television.5

Sources: See footnotes for data. The method of the buy-to-build indicator comes from (Nitzan & Bichler, 2009)

What did we imagine Hollywood’s buy-to-build indicator would look like? Figure 1 shows how the indicator rose from the 1980s to the early 2000s. This rise in the indicator makes sense; this period of twenty years is frequently conceptualized as one of Hollywood’s big waves of business consolidation. During this period we have global firms acquiring film studios, — e.g., Sony buying Columbia in 1989 — merging film and television production under the same corporate parent — e.g., Disney buying ABC in 1995 — and creating one-stop shops for mass culture through conglomeration — e.g., the merger of America Online and Time Warner in 2000.

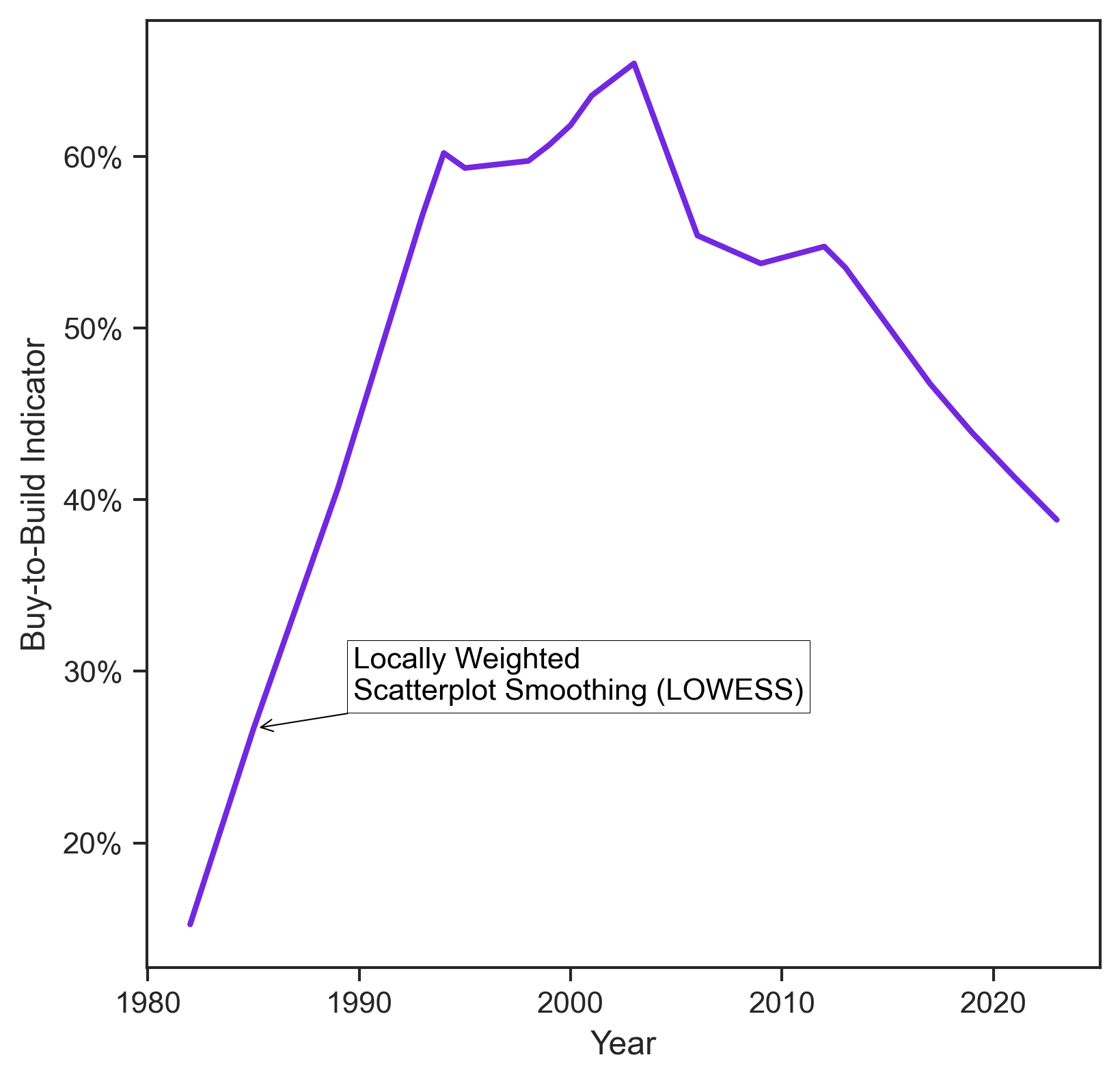

Interestingly, Hollywood’s buy-to-build indicator stagnates after 2000. Such a result might be surprising when we know there have been, since 2000, several mergers and acquisitions in Hollywood — including a big one, where Disney purchased 21st Century Fox in 2019. Figure 2 helps us see the curious situation better. It shows just the trend line from Figure 1.

In the next post, we try to unravel what has happened since 2000. There might be ceiling to what Hollywood to can “buy.” Moreover, this ceiling is significant if Hollywood in the 2000s has hardly been keen to “build.”

[ TO BE CONTINUED ]

Footnotes

- I originally used this example in Chapter 2 of The Political Economy of Hollywood. A free pre-print copy is available here. ↩︎

- There is no fixed method to decide what counts as a “major” merger or acquisition. My method involved collecting everything that I could from the Institute for Mergers, Acquisitions & Alliances and mergers and acquisition announcements from newspapers, business magazines, and periodicals (via Factiva). So-called minor mergers and acquisitions could exist but they are hidden from my methods of empirical research. Moreover, private fixed investment is in the billions of dollars, which suggests that the trend of the buy-to-build indicator would only change if hundreds, or even thousands, of small mergers and acquisitions were included in the calculation. ↩︎

- The Excel sheet is available for download. ↩︎

- The BEA defines Private Fixed Investment this way: “Private fixed investment (PFI) measures spending by private businesses, nonprofit institutions, and households on fixed assets in the U.S. economy. Fixed assets consist of structures, equipment, and intellectual property products that are used in the production of goods and services. PFI encompasses the creation of new productive assets, the improvement of existing assets, and the replacement of worn out or obsolete assets.

The PFI estimates serve as an indicator of the willingness of private businesses and nonprofit institutions to expand their production capacity and as an indicator of the demand for housing. Thus, movements in PFI serve as a barometer of confidence in, and support for, future economic growth.” ↩︎ - The sum is produced from two BEA series (via FRED):

A. Private Fixed Investment in Intellectual Property Products: Entertainment, literary, and artistic originals: Theatrical movies (Y021RC1A027NBEA)

B. Private Fixed Investment in Intellectual Property Products: Entertainment, literary, and artistic originals: Long-lived television programs (Y022RC1A027NBEA) ↩︎

References

Bagdikian, B. H. (2004). The New Media Monopoly. Beacon Press.

Balio, T. (1993). Grand Design: Hollywood as a Modern Business Enterprise, 1930-1939 (No. 5). New York: C. Scribner.

Bordwell, D., Thompson, K., & Staiger, J. (1985). The Classical Hollywood Cinema: Film Style & Mode of Production to 1960. New York: Columbia University Press.

Christensen, J. (2012). America’s Corporate Art: The Studio Authorship of Hollywood Motion Pictures. Stanford, California: Stanford University Press.

Cook, D. A. (2000). Lost Illusions: American Cinema in the Shadow of Watergate, 1970-1979 (C. Harpole, Ed.) (No. 9). New York: C. Scribner.

Litman, B. R. (1998). The Motion Picture Mega-Industry. Boston, MA: Allyn and Bacon.

Prince, S. (2000). A New Pot of Gold: Hollywood Under the Electronic Rainbow, 1980-1989 (No. 10). New York: C. Scribner.

Nitzan, J., & Bichler, S. (2009). Capital as Power: A Study of Order and Creorder. New York: Routledge

Schatz, T. (2010). The Genius of the System: Hollywood Filmmaking in the Studio Era. University of Minnesota Press.

Wasko, J. (1982). Movies and Money: Financing the American Film Industry. Norwood, NJ: ABLEX Pub Corp.

Wasko, J. (1994). Hollywood in the Information Age: Beyond the Silver Screen. Austin, TX: University of Texas Press.

Wasko, J. (2003). How Hollywood Works. London: SAGE.